Fintech funding across Africa was down ~70% y/y in H1 2024. Here's what to watch.

Insights from Afridigest's updated Africa Fintech Transactions Database

The H1 2024 update of our Africa Fintech Transactions Database is finally here.

In it, you’ll find all the announced fintech deals tracked from Jan 1, 2022 to June 30, 2024.

That includes equity & debt fundraises and M&A deals. (In line with deal reporting best practices globally, it excludes grants.)

Be sure to scroll to the bottom of this email — premium subscribers will be able to download the database in Excel format there. 🙏🏽

In H1 2024, roughly 60 fintech startups across Africa announced raising ~$340M in risk capital (equity and debt) over 66 transactions.

Total fintech funding raised across the continent in the first half of 2024 was down ~70% compared to the same period last year. But the number of deals announced held firmer, declining only 24% compared to H1 2023.

Here’s a quick summary of fintech funding across Africa in the first half of the year:

Key trends to watch:

Market bottom? African fintechs raised ~$340M in H1 2024, down from ~$1.1B in H1 2023 and $1.5B in H1 2022. It feels like we’re closer to the end of the downturn than the beginning and I’d wager that H1 2025’s total funding figure will be greater than $340M.

New normal? The average fintech deal size on the continent fell from $13M a year ago to $5M so far this year. This seems like right-sizing as efficiency and bang-per-buck is more top of mind for entrepreneurs and investors.

Rare mega-rounds. After years of multiple fintech mega-rounds in H1, only Nigeria’s Moove raised over $100M in H1 2024. There are probably a few more fintech mega-rounds to come over the next 12 months or so across the continent. Likely among them: the expected unicorn round of South Africa's TymeBank.

NEKS dominance. Nigeria, Egypt, Kenya, and South Africa (NEKS) accounted for 90% of fintech funding. But they only accounted for 70% of deals. While investors increasingly explore beyond these core markets, they’re core for a reason — and they dominate big-ticket deals.

Beyond the Big Four. Ghana, Senegal, Cameroon, Tanzania, Morocco, and Uganda are the emerging fintech markets to watch. Ghana and Senegal are already well recognized in fintech circles across the continent, but interesting developments are underway in the MUCT/‘Little Four’ countries: Morocco, Uganda, Cameroon, and Tanzania.

🚨 Early-stage Africa-focused tech startups: Apply today to be featured in the Afridigest Startup Spotlight. 🚨

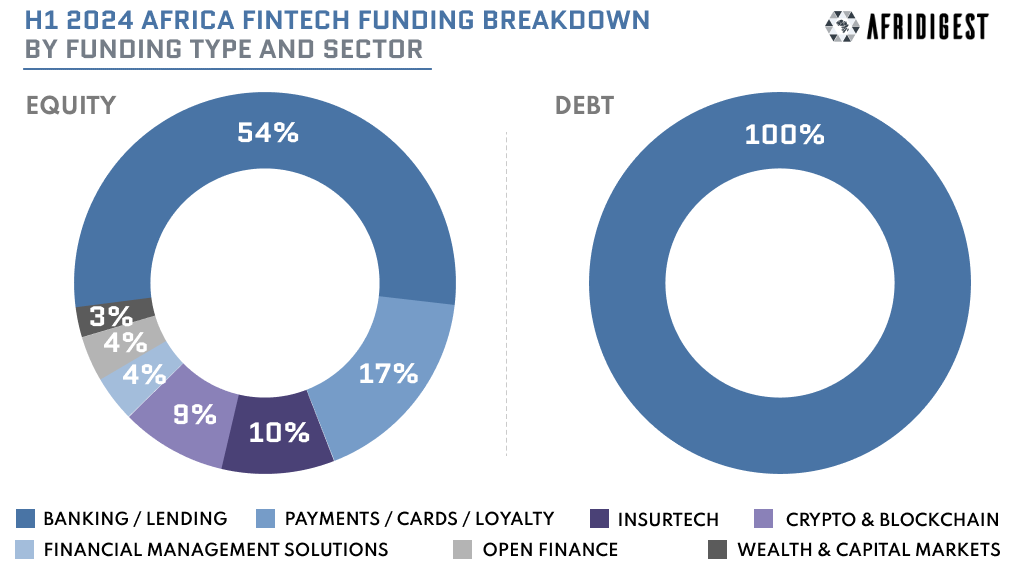

In terms of verticals, Banking/Lending led the way, accounting for $0.54 of every dollar of equity raised and all debt raised in 2023.

Not surprisingly, payments was second as it’s been in years past. But in a new development insurtech claimed the #3 spot.

Be smart: In H1 2024, the Banking/Lending vertical was driven by asset financing platforms like Moove, M-KOPA, Planet42, Watu, and Mogo Kenya.

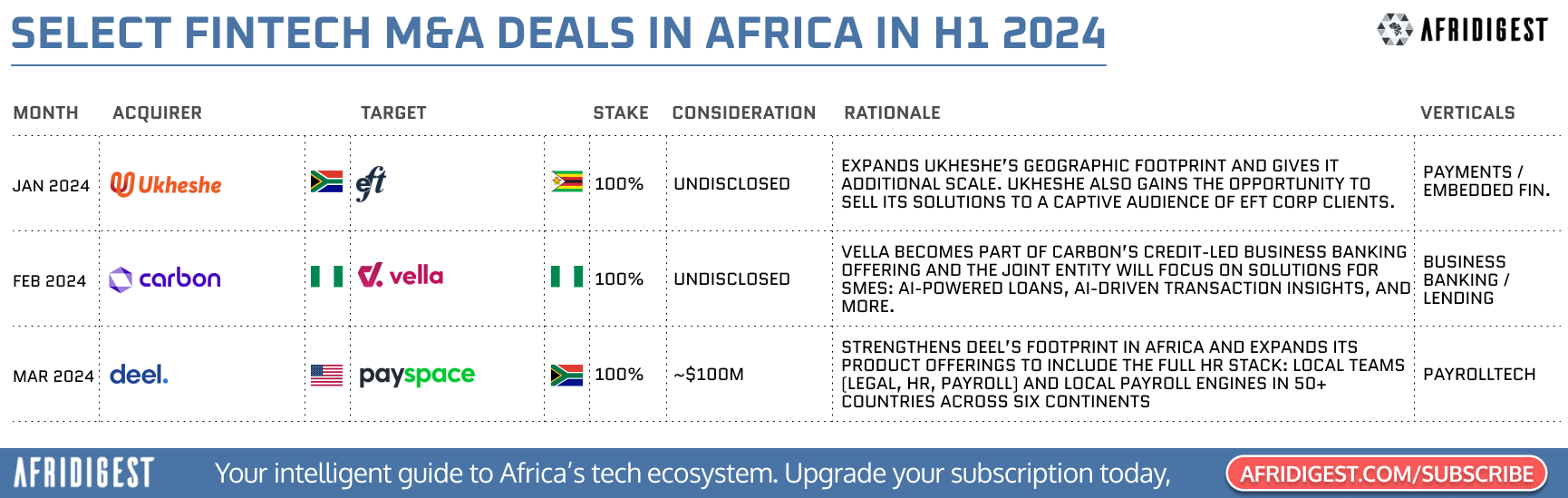

Beyond equity and debt financing, fintech M&A levels across Africa experienced a slight uptick with 18 deals announced in H1 2024, compared to 14 in the same period last year.

Here’s a quick look at select acquisitions:

That’s a sampling of what’s in the database.

If you're interested in:

Detailed sub-vertical-level information about fintech fundraises in Africa

Analyzing the continent’s fintech M&A landscape

Seeing the investors leading & investing in fintech rounds in Africa at a glance

Identifying who’s lending to African fintechs

Understanding African fintechs by country and funding stage

Then this database is for you.