Clever credit: How Nigerian startups are using data & distribution to de-risk lending

Africa-focused innovators can learn from the examples of three Nigerian companies that leverage unique data and distribution strategies to lend intelligently.

Afridigest is your intelligent guide to Africa’s tech ecosystem. We provide ideas, analysis, & insights for Africa-focused founders, executives, and investors.

This Saturday essay highlights three Nigerian startups leveraging unique/proprietary data and smart distribution strategies to improve credit underwriting and lower customer acquisition costs.

If you’re new here: welcome — an original essay like this goes out on Saturdays (occasionally), the Week in Review is sent on Mondays, and the Fintech Review goes out on Sundays.

International Women’s Day is next Wednesday and we plan to publish a special article then. For past essays and digests, visit the archive. And upgrade your subscription to support our work.

SIGN UP TODAY IF YOU’LL BE IN LAGOS 🙏🏽

» Sign up.

If you're in the US, Europe, or other places that enjoy relatively frictionless payments, widespread digital banking, & readily available credit, it can be hard to appreciate the realities of financial services in emerging markets across Africa & elsewhere.

In Nigeria, for example, ~55% of adults don't have bank accounts; in Egypt, cash accounts for almost 3/4ths of the country's overall payment volume; and in sub-Saharan Africa as a whole, bank credit is generally hard to come by for all but the largest and most well-connected institutions and individuals.

I've written several times before that the appetite for credit is virtually unlimited across African markets, so I'll focus on lending here.

Success in lending, in my view, depends on 3 Ds: data, distribution, and “dollars” (i.e., balance sheet access — preferably in local currency to guard against FX risks).

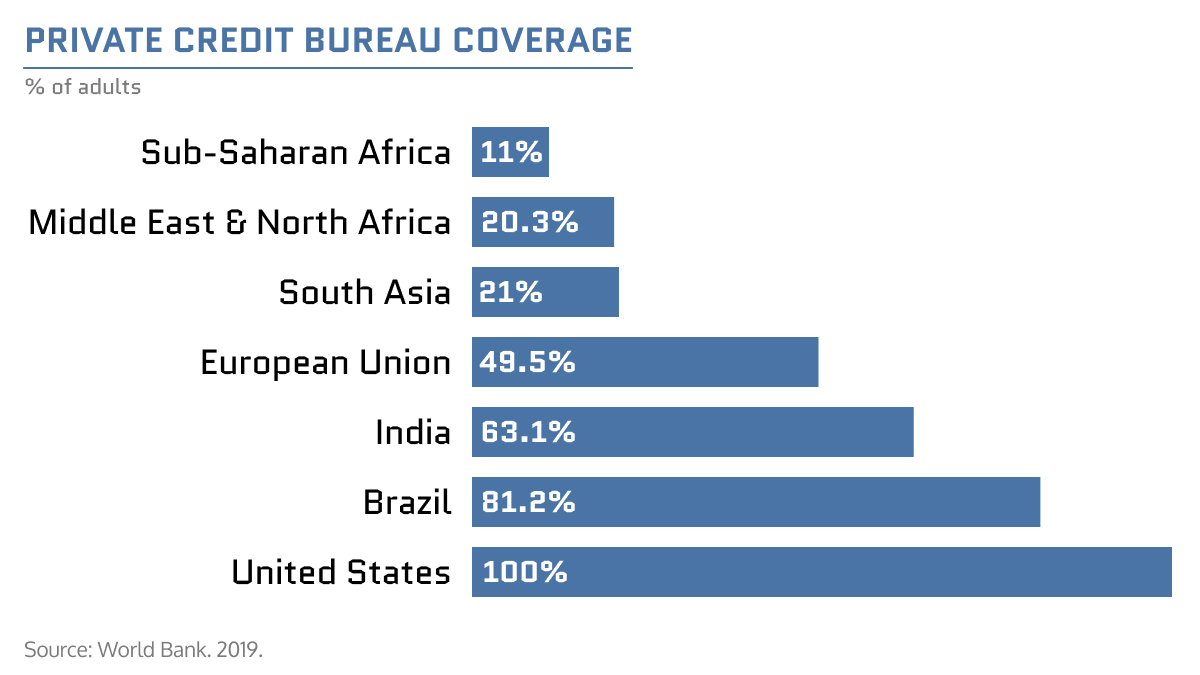

But with so many unbanked and underbanked people across the African continent, formal credit data largely doesn't exist and centralized credit bureaus tend to be in their infancy.

That's part of why risk-averse incumbent banks in Africa generally avoid SME/consumer lending despite their distribution advantages.

And while a variety of digital lenders have filled the void with 'alternative' credit models that sometimes rely on phone call logs, internet browsing history, messaging habits, daily location patterns, social media behavior, and the like to assess creditworthiness, they generally don't have existing distribution and they rely, in many cases, on VC funding to acquire customers.

But a number of startups are attacking the space differently. They use unique and/or proprietary data to build smart credit models while enjoying in-built distribution that lowers customer acquisition costs.

Here’s a look at three Nigerian startups doing just that.

Let’s jump in 👇🏽