Save now, buy later: an emerging fintech model

Plus an interview with Tobi Odukoya, CEO & Co-Founder of Nigerian SNBL platform CDcare

Afridigest provides ideas, analysis, & insights for Africa-focused founders, executives, and investors.

This post highlights an emerging business model worth paying attention to — SNBL — and includes a brief interview with one of the practitioners in Africa’s SNBL space.

If you’re new, welcome 🙌🏽 — you’ll receive an essay or another original piece on (some) Saturdays, a fintech-focused digest on Sundays, and a weekly digest every Monday. For past essays and digests, visit the archive.

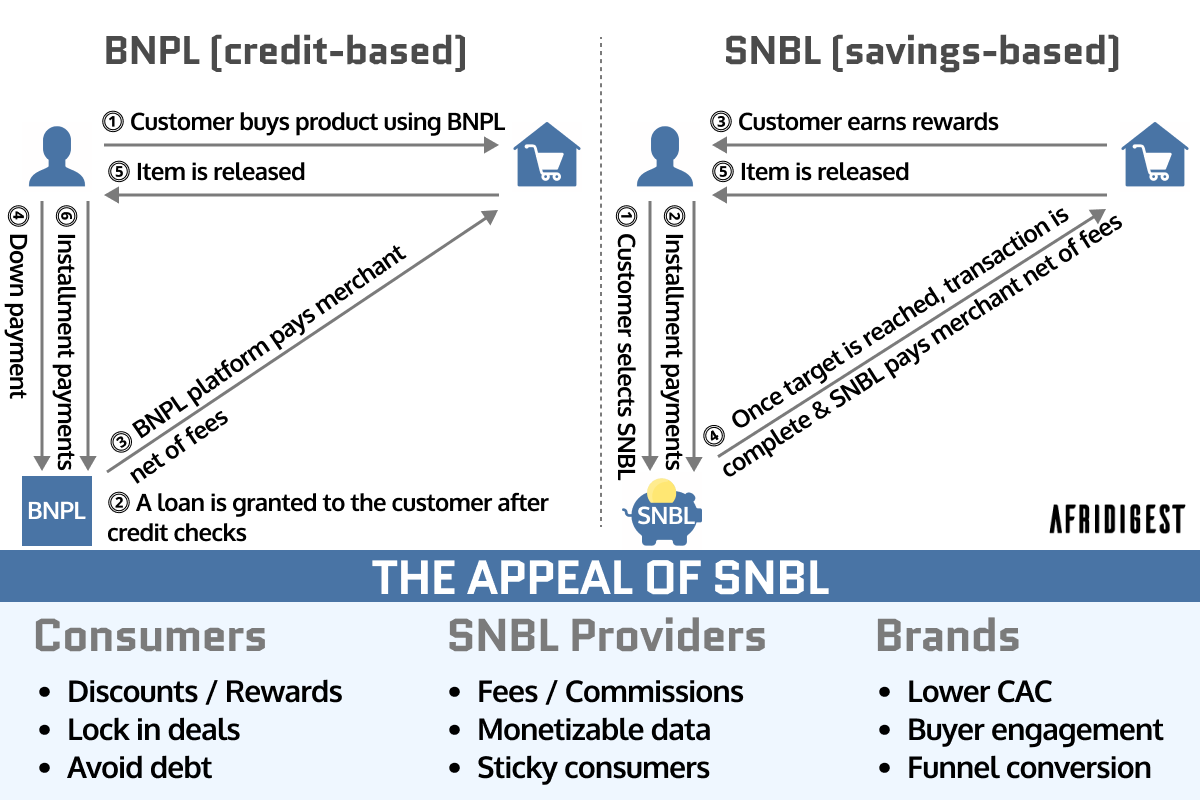

You're probably familiar with the terms ‘buy-now-pay-later’ and BNPL by now.

In recent years, the model has taken off worldwide and produced a number of global juggernauts like Klarna — once one of the world's most valuable fintechs.

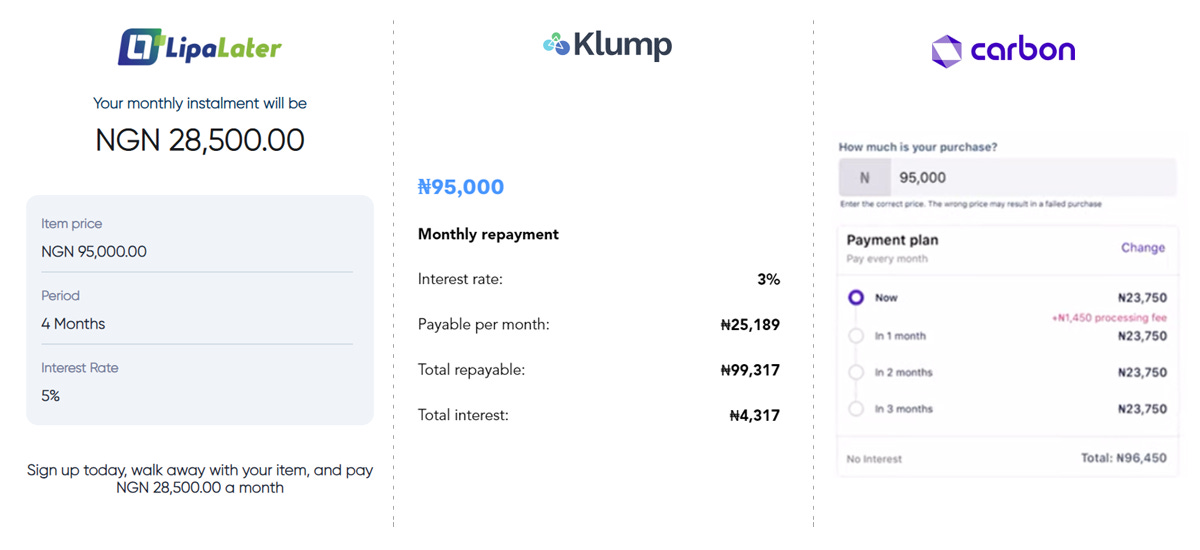

Across Africa, BNPL solutions are increasingly common across the continent’s major tech hubs too, with offerings from Lipa Later, Aspira, Safaricom, and others in Kenya; Carbon, CredPal, Klump, and others in Nigeria; Shahry, ValU, MNT-Halan, and others in Egypt; and PayFlex, PayJustNow, Float, and more in South Africa.

The typical BNPL model gives customers instant access to an item after a credit check and a 20-25% down payment, with the outstanding balance split into multiple equal installments payable over a pre-defined time period.

And while some BNPL providers don’t charge interest, many do, and most platforms charge substantial penalties for late payments and some form of processing fees.

But despite the rapid adoption of BNPL globally, today there are an increasing number of questions about the sustainability of the model. Klarna, for example, saw its valuation cut 85% from ~$46 billion in June 2021 to ~$7 billion in June 2022 as losses tripled.

Against that backdrop, there’s a new breed of innovators who view BNPL and related credit-driven models as undesirable; they argue that, aside from questions of commercial viability, these models lead to impulse-driven overspending, debt traps, and other negative outcomes.

So they’re innovating around savings and embedding new functionalities into the online retail experience.

The sector's called 'save now, buy later' (SNBL). And it’s exactly what it sounds like.

Unlike the BNPL model where consumers pay a down payment and receive the item immediately, under SNBL models, consumers choose an installment plan and make payments, but generally don’t receive the item until they’ve paid the full purchase price.