How ride-hailing apps become super apps: The Grab & Gojek playbook

Southeast Asia's Gojek & Grab have laid out a super app playbook to follow for ride-hailing startups in emerging markets

Afridigest provides ideas & analysis for startup founders, operators, and investors across Africa and beyond.

This essay is the second in a series about super apps — it follows up the WeChat focused essay, 'Why super apps are proliferating across emerging markets.’

If you’re new, welcome 🙌 — you’ll receive 2 weekly Afridigest emails: an original essay (on Saturdays) and the weekly digest (every Monday). For past essays and digests, visit the archive.

Subscribe here:

In the ASEAN region, there is a slew of companies valued at over $100 million USD. This chart from Cento Ventures provides a non-exhaustive overview:

At the top of the list, rubbing shoulders with publicly-traded Sea Limited, are two super apps: Grab & Gojek. Unlike China’s WeChat which began as a messaging service (see the previous article: Why super apps are proliferating across emerging markets), Gojek & Grab both offer ride-hailing as their core service and have become ‘must-own’ apps, not least due to the region’s underdeveloped public transport infrastructure (outside of Singapore).

Together, they’ve raised ~$15 billion dollars from some of the biggest names in tech — Gojek is backed by Google, Tencent, and JD.com, while Grab’s investors include Microsoft, SoftBank, and Didi Chuxing. This war chest hasn’t been sitting idle; over the past several years, the two companies have burnt through billions as they’ve jostled to establish dominant positions across the region and outcompeted world-class rivals.

In early 2013, Uber entered the region and spent, according to the Wall Street Journal, ~$200 million annually to compete against the young upstarts. Ultimately, however, in March 2018 Uber sold its Southeast Asia operations to Grab, receiving a 27.5% stake of the company in return.

“We used to be called the Uber of Southeast Asia, until we acquired them.” — Hooi Ling Tan, Co-Founder of Grab

Today, according to App Annie data, both apps have over 170 million downloads, suggesting that they’ve penetrated nearly one-third of the ASEAN region’s population. Furthermore, Gojek is estimated to have ~2 million drivers and ~500,000 merchants to Grab’s ~3 million drivers and ~200,000 merchants.

Although Grab President Ming Maa told the Financial Times at the end of 2019 that “our current business plan does not require any additional capital being raised,” the company went on to raise ~$1.06 billion in 2020 (so far). Not to be outdone, Gojek itself has so far raised ~$1.6 billion in 2020, including a June investment from Facebook and PayPal focused on the company’s fintech service, GoPay.

A brief history

Founded in 2010 in Indonesia as a motorcycle ride-hailing & courier service call center, Gojek launched its app in 2015. And today, the company also operates in Thailand, Vietnam, and Singapore.

Grab, on the other hand, was launched in 2012 in Malaysia, where it started with a taxi-hailing app, and today operates in Singapore, Indonesia, Thailand, Vietnam, Philippines, Myanmar, and Cambodia as well.

Despite this international expansion, Indonesia, the single largest market in the region, is the epicenter of both companies’ activities and their main battleground; the country accounts for over 90% of Gojek’s city operations and ~66% of Grab’s.

Below is a timeline of selected key moments in Gojek’s history:

And here’s a look at the various services Gojek offers today:

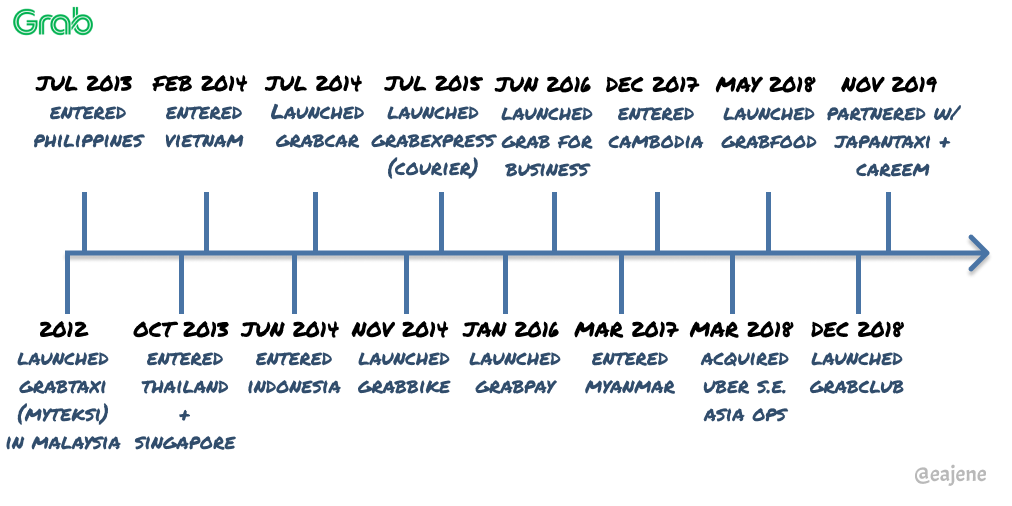

Similarly, here’s a timeline of selected key moments in Grab’s history as well as a look at the various services it offers today:

And here’s a look at the various services Grab offers today: